Plastic Taxation in Europe: Update 2024

Key Facts

- In 2021, European Union (EU) introduced a plastic levy on non-recycled plastic packaging waste to reduce waste and fund EU budgets, with rates set at EUR 0.80 per kilogramme.

- Recent changes across MS include the introduction of new taxes, adjustments to existing taxes, and the implementation of extended producer responsibility (EPR) systems.

- Examples of recent changes include Germany’s introduction and postponement of the national plastic tax, Portugal’s extension of single-use packaging contributions with modified rates and exemptions, and Poland’s introduction of fees on certain single-use plastics and establishment of a deposit-refund scheme.

Tackling plastic pollution and waste at the European and national levels

The European Union’s legislation regulating plastic waste

The issue of plastic packaging waste has been at the forefront of policy thinking in Europe in the recent years. On 1 January 2021, the European Union (EU) introduced a levy based on the amount of non-recycled plastic packaging waste produced by each EU Member State (MS). This “plastic levy” is designed to reduce the proliferation of non-recycled plastic waste while concurrently funding the 2021–2027 EU budget against the backdrop of the increased spending arising from the pandemic. Each MS is required to pay a levy determined by multiplying a rate of EUR 0.80 per kilogramme by the weight of non-recycled plastic packaging waste. While some MS have been paying the levy out of their national budgets, others have introduced (or are looking to introduce) new taxes, duties, charges, fees, or contributions on plastic products, or have extended (or are considering extending) existing schemes to tax plastic products as well.

Furthermore, since 3 July 2021, the EU has banned certain single-use plastic products such as cotton bud sticks, cutlery, plates, straws, stirrers, and sticks for balloons under EU Directive 2019/904 on Single-Use Plastics (SUP). For other single-use plastics, the SUP Directive has introduced several measures, such as waste management and clean-up obligations for producers (such as the Extended Producer Responsibility Schemes), which aim to reduce these products. Under Article 8 SUP Directive, the MS need to ensure that the producers of single-use plastic products cover the costs of cleaning up litter resulting from these products and the subsequent transport and treatment of that litter. This provision has resulted in some MS introducing the so-called “littering levy”.

Additionally, the EU has introduced rules on packaging and packaging waste to harmonise national measures that aim to tackle the problem of increasing quantities of packaging waste. One of the SUP Directive’s requirements is to ensure that producer responsibility schemes are established for all packaging by the end of 2024.

Furthermore, a proposal for a Packaging and Packaging Waste Directive (PPWD) is currently being considered by the European Parliament and the Council of the EU. This new revised legislation will increase the pressure on the MS to harmonise Extended Producer Responsibility.

Thus, these developments create a very complex and complicated system where plastic producers, distributors, and consumers need to be aware of the numerous measures in each country, as these differ across Europe

Plastic taxation and levies in the member states

In the recent years, the MS have started to implement the European Waste legislation as well as their own national rules and measures to tackle the issue of plastic waste. Currently, there exist various combinations of laws and levies and taxes applied differently by each MS. The existing measures can be categorised into 4 categories:

- Plastic and Plastic Packaging Taxes (PPT);

- Regulatory bans and marking requirements for single-use plastics (SUP);

- Extended Producer Responsibility (EPR) fees and licence requirements for waste disposal systems;

- Littering levies for the costs of cleaning up litter.

Among the MS that have implemented some kind of plastic tax, the tax design varies greatly. Some focus on packaging (i.e. both plastic and non-plastic packaging), while others are narrower in scope, targeting single-use or non-reusable plastics only. Some MS are imposing a tax on domestic and foreign-sourced plastic products, whereas others are relying on an excise tax mechanism to exclusively target foreign-sourced plastic products. The list of exempt products also differs from one MS to another. Crucially, the rate of tax varies across the MS, with some choosing not to levy a tax at all.

What has emerged is a patchwork of uncoordinated national and regional rules that require careful examination and navigation by enterprises operating in multiple MS. The EU is aware that an uncoordinated approach, fragmented rules, and vague requirements are creating barriers within the internal market and additional costs for economic operators. However, since taxation is a national competence and passing any tax legislation requires unanimity at the Council of the EU level, it is highly unlikely that we will see an EU Plastic Taxation Directive anytime soon. The only measure that the EU is currently undertaking is the PPWD, which is meant to harmonise more the EPR requirements as well as other requirements on recyclability and labelling.

Challenges for enterprises

Enterprises will do well to stay abreast of developments and track the evolving regulatory and tax landscape so as to ensure that they do not fall foul of the applicable national rules and are not subject to enforcement proceedings or financial penalties for non-compliance.

In terms of business operations, the existence of a plastic tax and other levies can have wide-ranging implications for an enterprise’s internal processes and procedures. As a preliminary step, the enterprise will need to familiarise itself with the types of plastic taxes and levies that are imposed in each country in which it operates and ascertain which of its local entities is liable to pay the tax or levy. Depending on which entity within the supply chain is liable, there may be invoicing and pricing implications to consider. Thereafter, the enterprise will need to identify the employees responsible for handling compliance and provide such employees with relevant training to enable them to adequately perform their duties. The enterprise’s tax and legal departments must also be prepared to support the additional compliance obligations. The enterprise must also be able to single out the types of materials or products that are subject to tax from within its supply chain, and its enterprise risk management systems must also be adapted to handle these compliance requirements.

To help companies make sense of this rapidly growing area of taxation, WTS Global has invested in building up its competence and expertise in this field to provide both national and cross-border support. This current report serves as a reference to aid companies in navigating tax issues arising from the manufacture, importation, distribution, or use of plastic products, and also to initiate deeper thinking on how plastic value chains can become more circular.

Summary of the most important changes

Across the EU, MS have implemented significant updates to plastic taxes and levies in recent years. From 2023 to 2024, several countries have introduced various measures, including new taxes, EPR systems, and changes to existing regulations concerning single-use plastics and related products. See below for the major highlights and find more in-depth information in the detailed country descriptions. overviews.

Bulgaria introduced a new product fee for certain single-use plastic products as part of the EPR. The exact fee amount has yet to be determined. Under the new Ordinance, producers of certain single-use plastic products must file yearly reports and the first report was due on 31 March 2024.

Denmark increased the rate of the excise duty on carrier bags and disposable tableware in January 2024.

Germany will be implementing a national plastic tax from 1 January 2025, and has introduced an annual levy on single-use plastics predominantly for disposable food packaging. Originally scheduled to take effect on January 1, 2024, the implementation date has been pushed back to most likely 2026.

The UK has rolled out a new tax rate for PPT, effective since 1 April 2024, following the introduction of a penalty regime in 2023.

Hungary introduced a new EPR system alongside the existing Environmental Product Charge (EPC). The new EPR have applied since 1 July 2023 to packaging products and other plastic items (it also covers other product categories such as electrical and electronic equipment, etc.), with fee rates dependent on the product type and taxpayer profile.

Italy has postponed the PPT’s implementation until 1 July 2024.

Latvia has differentiated foam polymer and polystyrene foam from other plastics raw materials with a higher natural resources tax.

Lithuania has enacted changes to already existing pollution by adjusting tax rates, exemptions, and other regulations that will become effective from 1 January 2025.

The Netherlands has adjusted waste management contributions for plastic packaging and extended the EPR fee to include cigarette filters.

Poland introduced legislation in 2023 for fees on certain single-use plastics and established a deposit-refund scheme.

Portugal extended the scope of single-use packaging contributions, adjusted rates, and introduced new exemptions in the State Budget Law for 2024.

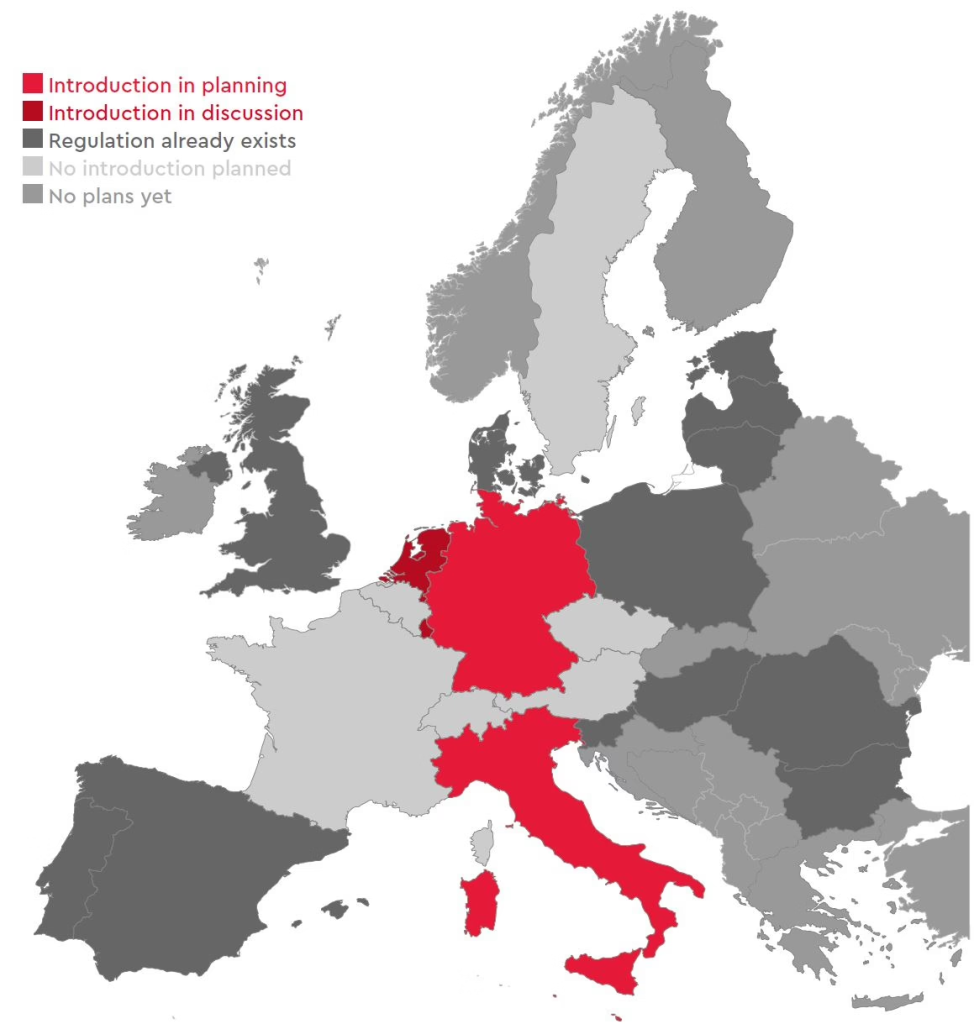

Overview of the State of Implementation

Click on the country name for a summary of some of the significant measures proposed or adopted by European countries (including Member States) to impose a financial cost on the use of plastic products.

Austria

Belgium

Bulgaria

Czech Republic

Denmark

Estonia

France

Germany

Hungary

Italy

Latvia

Lithuania

Luxembourg

The Netherlands

Poland

Portugal

Romania

Slovenia

Spain

Sweden

Switzerland

United Kingdom

(Source: https://wts.com/global/publishing-article/20240508-plastic-taxation-europe-update-2024~publishing-article)